Summary

Today’s market session was a rollercoaster of earnings surprises, policy shocks, and renewed volatility. Nvidia jumped over 5% after reporting better-than-expected Q1 results and a solid Q2 outlook. Meanwhile, semiconductor stocks came under fire as the U.S. targeted software exports to China, escalating tech tensions. In a late-day development, the U.S. Court of International Trade ruled Trump’s sweeping tariffs illegal, sparking a bounce in stocks and futures. All eyes remain on AI, chips, and policy shifts as macro data continues to strengthen.

Market Watch

Economic Data

- 📈 US PRELIM GDP 8:30 AM ET: May 29, 2025

- 📈 US UN-EMPLOYMENT CLAIMS 8:30 AM ET: May 29, 2025

- 📈 US CORE PCE PRICE INDEX: May 30, 2025

📚 Deep Dive 📚

Soft data firming, semiconductors under fire, another 0-DTE rollercoaster ride, an NVDA beat, and a last minute tariff halt. What a day!

Let’s break it down:

Soft Data Rises, Fed Minutes Fall Flat

While partisan debates continue in the background, the market is beginning to lean on tangible data again. Three regional Fed surveys (Richmond Manufacturing, Richmond Business Outlook, and Dallas Services) beat expectations, adding to a growing trend of ‘soft’ data aligning with resilient ‘hard’ data. For the first time in a while, the economic backdrop is starting to confirm the strength we’ve seen in consumer and corporate activity since the pandemic.

Meanwhile, the FOMC minutes were a nonevent—a bland echo of past statements, offering no surprises and no forward guidance worth noting. Markets shrugged.

💣 Semiconductors Hit Again – U.S. Tightens Grip on China

The real bombshell came from The Financial Times:

The Trump White House is now pushing to restrict U.S. chip design firms from selling to China, including heavyweights like Cadence (CDNS), Synopsys (SNPS), and Siemens EDA. The Commerce Department has already sent letters to these firms, requesting a halt in shipments to Chinese customers—a sign of more aggressive export control measures in the pipeline.

“Commerce has suspended existing export licenses or imposed additional license requirements while the review is ongoing.”

– U.S. Commerce Dept.

The implications are massive. These companies create the software that powers semiconductor design—used in everything from Nvidia and Apple chips to basic components. If enforced, this would represent a major escalation in the U.S.–China tech cold war.

Nvidia (NVDA), which already faced restrictions on its H20 chips to China in 2023, was once again in the spotlight. CEO Jensen Huang has repeatedly criticized these restrictions, calling them ineffective and harmful to innovation.

Markets didn’t take it well. Stocks fell on the headlines (although recovered), with small caps and the Nasdaq hit hardest. It’s clear: the U.S. is doubling down on efforts to choke off China’s domestic semiconductor push, and investors are recalibrating fast.

⚖️ 0-DTE Chaos and Market Whiplash

The morning session saw sellers hit early, especially in the Asia session, before European buyers lifted stocks into the U.S. open. But once Europe closed, U.S. indices spiked, with the Nasdaq briefly reclaiming green.

Then came the real action.

At 2:40 PM ET, stocks plunged with no obvious headline, a move attributed to an aggressive unwind of long 0-DTE call positions. But in classic 2025 fashion, panic call-buying kicked in moments later, pushing the Nasdaq right back up.

📉 Bonds, Bitcoin, and Commodities

- Yields rose 2–3 bps across the curve, with a slight tilt toward the long end. The 30-year briefly breached 5.00% before reversing lower.

- 2025 rate cut expectations declined, while 2026 cut odds increased—clearly a shift in the forward curve.

- Bitcoin fell hard, retracing recent gains back to the $108,000 support zone.

- Oil closed green but remains well below its post-OPEC+ highs.

- Gold dipped slightly, closing near $3,300 after a volatile session.

- The U.S. dollar strengthened, especially against the yen, dragging metals and crypto lower.

NVDA Earnings Beat:

Nvidia reported its Q1 FY25 earnings with revenue totaling $44.1 billion, slightly beating expectations of $43.29 billion. Adjusted earnings per share came in at $0.96, ahead of the $0.93 estimate, while adjusted gross margin landed at 61%, notably below the expected 71%. The data center segment, a key growth driver, delivered $39.1 billion in revenue, nearly matching the $39.22 billion forecast. Compute revenue came in lower than expected at $34.16 billion (vs. $35.47B est.), while networking revenue surprised to the upside at $4.96 billion, beating the $3.45 billion estimate. Looking ahead, Nvidia guided Q2 revenue to $45 billion ±2%, just under the $45.5 billion consensus.

Stock is up +5% in after hours trading.

What Did GAR Do Today?

Options Recap:

We held firm on our three open positions through another day of relentless continued chop on our premiums. GOOG and AMZN were on our radar all session—we finally got the break overnight, so we’ll be watching closely for a clean follow-through. No chasing here though. TSLA and HOOD are starting to mount a comeback, while HIMS remains the wildcard—unless it reclaims $65 tomorrow and Friday, time is running out.

Futures Recap:

U.S. Session:

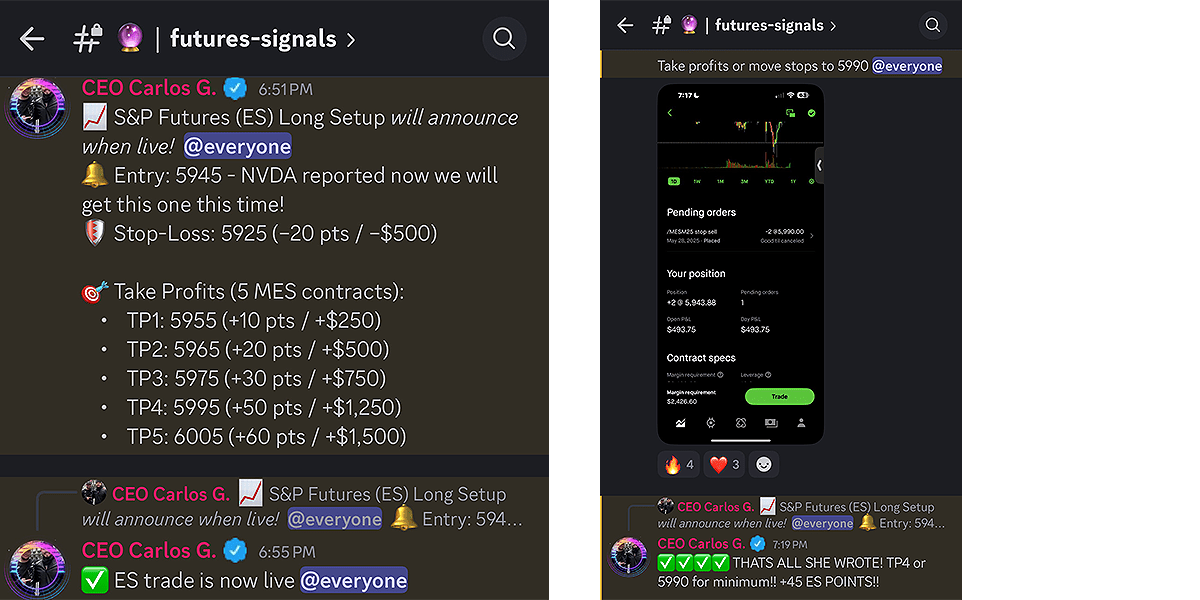

- We took a long entry on S&P Futures at 5945 but were quickly stopped out for a –20 point loss. The price action was choppy and directionless—classic no-follow-through day. We stuck to our risk management plan and didn’t force anything.

Asia Session (Tonight):

Textbook setup, flawless execution. We went long at 6:55 PM ET and locked in +45 points within 25 minutes. One of the cleanest trades of the week so far—great timing, great patience, great reward.

🔍 Narrative Watch: CEO Spin Incoming?

With macro uncertainty fading and U.S. policy clarity sharpening, the question remains—will high-profile CEOs and their media allies finally acknowledge the obvious?

Economic data is firm. The Fed is on hold. The government is actively reshaping tech policy. So how will corporate America respond?

We’re already seeing a subtle shift. The era of vague “cautious optimism” may give way to a new acronym-heavy narrative—“TACO,” or “Tech, AI, Chips, Optimization.” Whether this catches on or not, one thing’s for sure:

The market is forcing people to face reality—whether they’re ready or not.

📌 Final Thoughts:

- U.S. economic data is stronger than expected

- The semiconductor sector is squarely in the geopolitical crosshairs again

- 0-DTE options are driving intraday chaos—expect more of the same

- NVDA remains the AI market barometer

- Watch for narratives to shift as soft data keeps firming

TARIFF NEWS TONIGHT:

In a significant legal rebuke, the U.S. Court of International Trade ruled on May 28, 2025, that former President Donald Trump overstepped his authority by imposing sweeping tariffs under the International Emergency Economic Powers Act (IEEPA) of 1977. The court unanimously invalidated the so-called "Liberation Day" tariffs, which included a 10% duty on all imports and higher rates on goods from countries like China, Mexico, and Canada.

The judges determined that persistent trade deficits do not constitute the "unusual and extraordinary threat" required to invoke IEEPA, emphasizing that such broad tariff powers reside with Congress, not the executive branch. The ruling, stemming from the case V.O.S. Selections, Inc. v. Trump, was hailed by small businesses and legal experts as a victory for constitutional checks and balances. While the Trump administration has filed a notice of appeal, the decision marks a pivotal moment in delineating the limits of presidential power in trade policy.

Nasdaq Futures are +2% over night on the news.

Stay tactical and stay ready, — Carlos

GAR Capital