Summary

NVIDIA’s Q1 FY2025 earnings confirmed its leadership in the AI-driven bull cycle, reporting a clean beat across revenue, earnings, and key growth segments. Data center revenue soared 73% YoY to $39 billion, pushing total revenue to $44.1 billion. The stock jumped 4.29% in after-hours trading, breaking above resistance levels. GAR Capital raised its 12-month price target to $150–153, citing strong fundamentals and continued AI demand.

Economic Data

- 📈 US CONSUMER PRICE INDEX : May 30, 2025

📚 Deep Dive 📚

NVIDIA Earnings Recap – Q1 FY2025

“Still the AI king. Still the growth king."

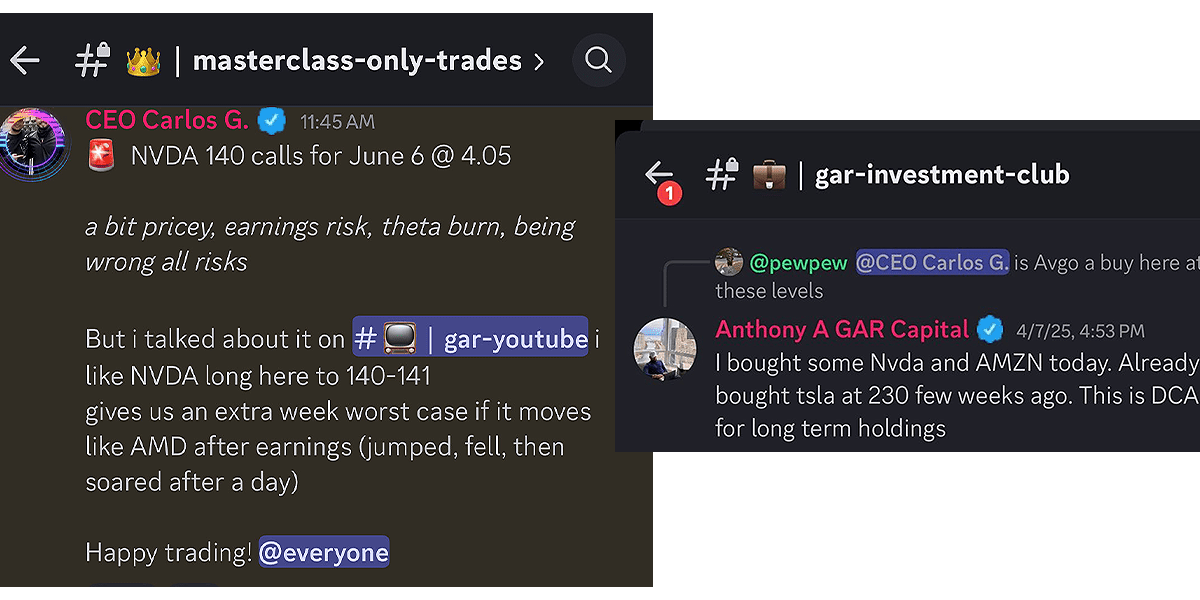

✅ We Called It.

We told our masterclass students. We told our YouTube subscribers. We posted it on the Discord watchlist. NVIDIA (NVDA) and the entire semiconductor sector were setting up for a bullish move—and tonight, that thesis got confirmed.

Don't forget our dip buy on April 7th as well.

After reporting blockbuster fiscal Q1 2025 earnings, NVIDIA surged 4.29% in after-hours, trading above $140 per share. Once again, the market is rewarding strength—and make no mistake, NVDA is still the leader of this AI-driven bull cycle.

💥 Earnings Highlights:

- EPS: $0.96 vs. $0.93 expected

- Revenue: $44.1 billion vs. $43.31 billion forecast

- Data Center Revenue: $39 billion (+73% YoY)

- Gaming Revenue: $3.8 billion (up 48% sequentially)

- Gross Margin: 75%

- YoY Revenue Growth: 114.2%

This was a clean beat across the board, with growth metrics that continue to dwarf every other name in the MAG7 lineup. The most important line item? Data center revenue at $39 billion—fueled by accelerating demand for AI infrastructure.

🚀 After-Hours Reaction:

- NVDA popped +4.29% post-earnings

- Closed after-hours at $140.59

- Broke above resistance on strong volume

- Options traders are pricing in more upside into summer

🎯 Our View: Price Target Raised

We’ve long said NVDA’s fair value is around $120/share without a growth premium—but this quarter proved that premium is not only justified, it may be expanding.

New 12-month target:

📍 $150–153 — new all-time highs well within reach during a potential summer rally.

We’re not making wild claims. We’re basing this on:

- Breakout earnings performance

- Strong forward guidance (Q2 est. $45B in revenue)

- Industry leadership in AI, gaming, data centers, and now robotics

- CEO Jensen Huang’s clear vision: “AI is growing faster than the internet, mobile, or cloud ever did.”

📉 Risks on the Radar:

- Geopolitical drag from China data center restrictions

- Supply chain bottlenecks

- Competitive pressures in AI and enterprise

- Macro volatility could affect high-beta names (NVDA’s beta: 2.11)

But none of these risks are new. And tonight, the market showed it’s still willing to pay a premium for real growth.

🧠 GAR Capital Masterclass Got It Right

This wasn’t luck. This was preparation.

We saw the setup. We traded the calls. We informed our community weeks ago that NVDA was a key leader to watch.

We don’t chase headlines. We build conviction and position accordingly. Tonight’s report confirms that thesis.

Looking Ahead:

- Q2 revenue guidance: $45B ± 2%

- Continued expansion into AI infrastructure, enterprise tools, and robotics

- Watch NVDA as the market barometer for AI momentum

Stay tactical, stay prepared, and as always—trade with a plan. Let’s make it a strong finish to the week, — Carlos GAR Capital