Summary

This week’s market rally was powered by a balanced jobs report, easing policy fears, and a major short squeeze—pushing the S&P 500 above 6000 for the first time since February. But it wasn’t all strength under the hood. Much of the move came from speculative, non-profitable names and short covering, raising questions about the rally’s quality. With yields rising, volatility dropping, and macro data softening, the next move hinges on whether the Fed sees enough to act—or stays patient.

Economic Data

📚 Deep Dive 📚

📆 Weekly Market Recap: Goldilocks Payrolls, 6000 S&P, and a Lower-Quality Squeeze

This week delivered a perfect blend of relief and confusion—policy uncertainty dropped, the Fed remained on pause, and yet markets kept pushing higher.

The headline?

Goldilocks payrolls + short squeeze = new all-time highs.

🧠 Sentiment Shift: Less Noise, More Clarity

Despite headline noise from Washington, policy uncertainty declined.

Friday’s payroll report had something for everyone:

🔹 Headline NFP beat expectations

🔻 Household data, revisions, and internals came in soft

Net takeaway: Balanced. Not hot enough to spook the Fed, not weak enough to signal recession. Even Goldman Sachs called it a “something for everyone” report—highlighting how soft data is finally catching up to hard numbers.

The market isn’t asking for perfection—it just wants predictability.

Interest Rate Expectations

- July rate cut odds dropped to 16% after the payrolls print

- Markets now price in 1.8 cuts through year-end

- Trump called for a full-point cut, but Powell stayed quiet

The Fed’s in no rush. The market is starting to believe them. But the question remains:

What’s the Fed waiting for now?

📈 Stock Market: A Cleaner Breakout, But Lower Quality

All major indices closed higher:

S&P 500 broke 6000, ending at 6000.35 for the first time since February. Small Caps and Nasdaq led the charge.

The rally was driven by:

- Positive China trade headlines

- Balanced payroll report

- A short squeeze across underperforming sectors

But let’s be honest: it was a lower-quality squeeze:

- Non-profitable tech, low momentum names, and shorted energy stocks led

- Bitcoin plays, beaten-down names, and HF VIP shorts all ripped

- Goldman flagged it as the worst day in nearly a year for HF VIP vs. Most Short baskets

- Even TSLA saw panic bidding within the Mag7 group

💥 Volatility & Flow

- VIX closed at 16 – lowest since February

Markets are calm—for now. But any shift in rate cut expectations could bring that calm to an end.

💸 Yields, Dollar & Commodities

- Treasury yields rose, especially on the long end

- The 30-year remained under 5%, but curve flattened significantly

- Dollar closed its lowest weekly level since July 2023

- Gold gained early but faded Friday

- Oil surged to a six-week high amid geopolitical risks and labor strength

Bitcoin stayed volatile:

- Fell to $101K early week then Recovered to $105K

- Closed slightly lower overall

📉 Macro Picture: Reflation Narrative Brewing?

- Growth surprise index: lowest since August 2024

- Inflation surprise index: lowest since August 2020

Historically, the Fed has cut rates with worse inflation and weaker growth than we’re seeing now

So the real question is: Are markets pricing in a slow-motion reflation? Or is the Fed still too hesitant with “not-bad-enough” data?

Either way, next week’s setup includes:

🟢 Technical strength

🟠 Fundamental division

⚠️ High macro sensitivity

🧾 What did GAR do This Week?

Our Options Desk navigated a choppy tape but still pulled out solid wins. Robinhood (HOOD) delivered the highlight of the week, with a +175% runner on the $70 calls, while Amazon (AMZN) rebounded strongly for a +40% gain. Palantir (PLTR) popped early with a +32% intraday move but faded by week’s end, burning remaining premium for those who didn’t lock in. Meanwhile, we strategically bought dips in HIMS and NVDA, which we continue to hold, alongside TSLA calls—all set for expiries in the next two weeks.

✅ Winners:

- HOOD 6/20 $70 Calls — +40% (runner hit +175%)

- AMZN 6/6 $210 Calls — +40%

❌ Loser:

- PLTR 6/6 $135 Calls — closed red despite a +32% intraday spike Tuesday

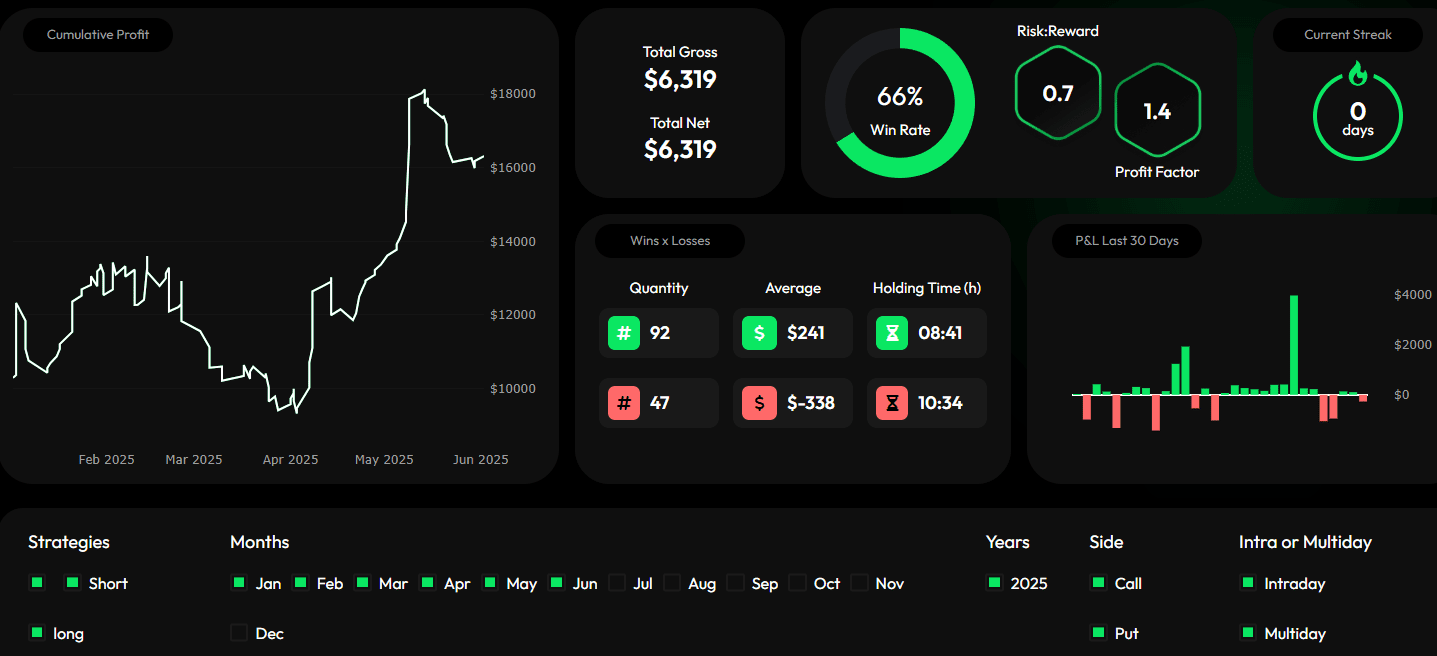

Here is a screenshot of our Options Trading Journal return on alerts YTD:

For our Futures Squad it was another tight, choppy week—but we stayed patient and ended green.

Weekly P&L (based on 5 micros):

- S&P 500 (MES): +35 pts → +$875

- Gold (MGC): –5 pts → –$250

🔒 Final Net: +30 pts / +$625

Tuesday’s long in the S&P made the week, while Friday’s push helped lock in more gains. Our losses were small, and risk was well-managed—exactly how we like it. June chop remains, but we're staying sharp and opportunistic.

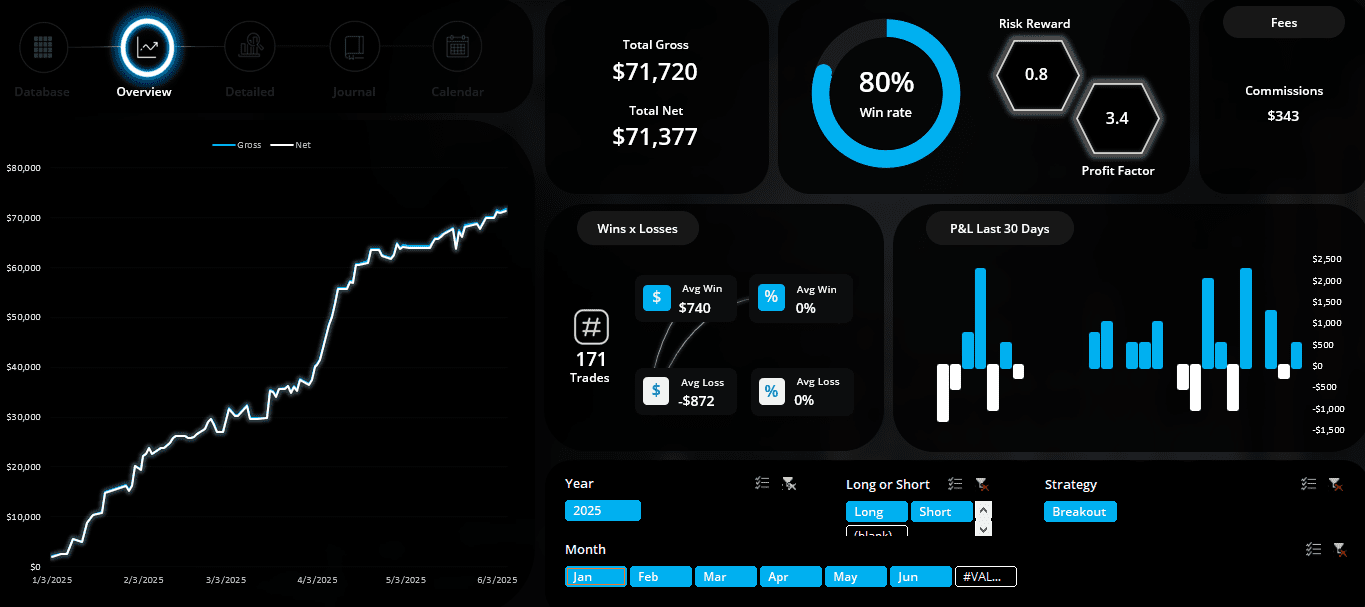

Here is a snapshot of our Futures Trading Journal YTD on alerts:

✅ Bottom Line

- Payrolls were “just right”—balanced and Fed-friendly

- S&P 500 broke 6000, but rally quality remains questionable

- Shorts got squeezed; the Fed stayed steady

- Yields climbed, VIX dropped, Bitcoin stayed chaotic

All eyes on next week’s macro data as we approach a sentiment pivot point.

Stay tactical. Stay disciplined.

We’ll be ready either way. – Carlos G

GAR Capital📒Trading Journal: Your Edge, Documented

All serious traders need a system—and our GAR Trading Journal is built for exactly that. Track entries, exits, P&L, and lessons learned in one place.

Included with Annual Memberships—because reviewing your process is how you sharpen your edge. Upgrade Here